3.1. ECONOMIC GROWTH

|

|

|

Economic growth is a positive change in the value of real GDP. We usually measure growth rates year on year. A negative value for economic growth means that the economy is contracting. We can distinguish economic growth into short and long run growth.

|

Long Run Economic growth

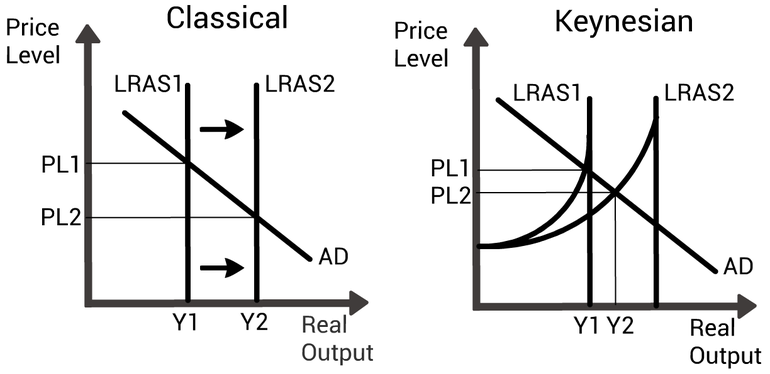

Long-run economic growth is where the productive capacity of the economy increases. This is a sustainable source of economic growth and can come about by a variety of different factors, such as an increase in technology, labour productivity rising etc. Changes to the supply side of the economy are key to the long run economic growth of the economy. This is why the government uses supply side policies. A diagram of this is represented below.

Long-run economic growth is where the productive capacity of the economy increases. This is a sustainable source of economic growth and can come about by a variety of different factors, such as an increase in technology, labour productivity rising etc. Changes to the supply side of the economy are key to the long run economic growth of the economy. This is why the government uses supply side policies. A diagram of this is represented below.

A classical and Keynesian diagram showing long run economic growth.

Short Run Economic Growth

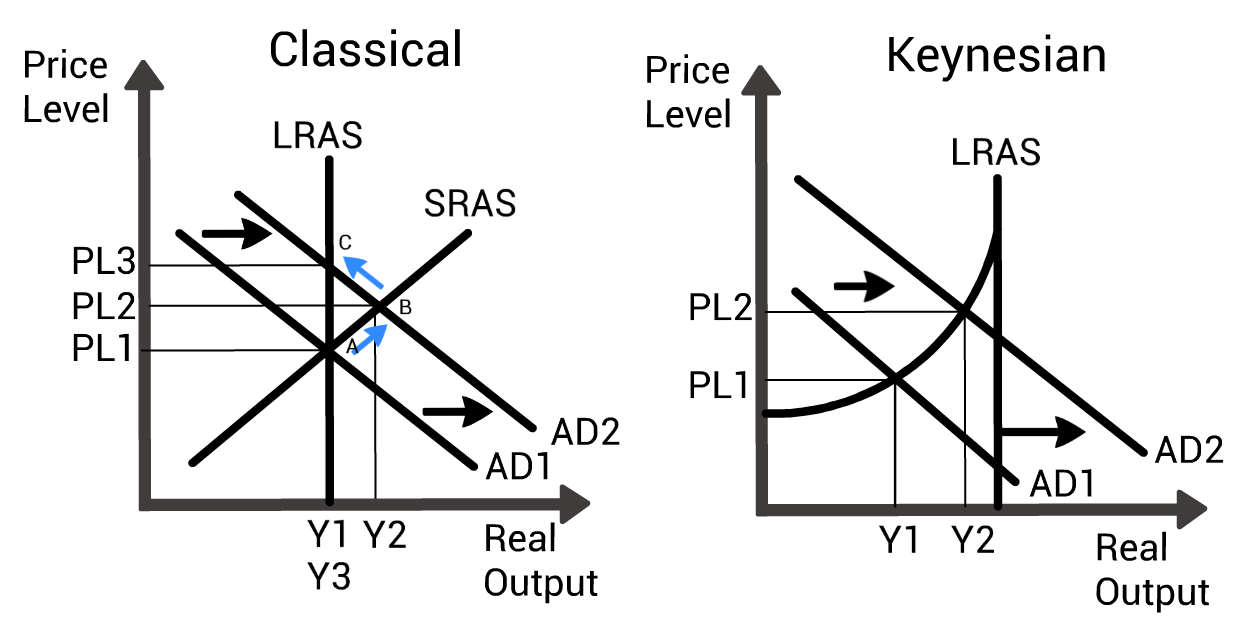

Short run economic growth is caused by a variety of different factors. These factors either affect SRAS or AD. For example, an increase in the level of confidence in the economy resulting in consumers consuming more and firms increasing their level of investment. This would result in a shift of AD to the right. In the short run this is accommodated by an increase in supply. However, if we subscribe to the classical economic thought we see that in the long run firms decide to increase their prices as they have to pay staff more for overtime and this results in a shift of the SRAS to the left. This means that we are at a new equilibrium where output is at the same level and the price level is higher (PL3). This is why this type of growth is short run economic growth. With the Keynesian view, if the economy has a negative output gap, the increase in aggregate demand causes the price level to rise and real output to also rise. If the economy was already producing its long run maximum of output, we would see no change in output and only an increase in the price level.

Short run economic growth is caused by a variety of different factors. These factors either affect SRAS or AD. For example, an increase in the level of confidence in the economy resulting in consumers consuming more and firms increasing their level of investment. This would result in a shift of AD to the right. In the short run this is accommodated by an increase in supply. However, if we subscribe to the classical economic thought we see that in the long run firms decide to increase their prices as they have to pay staff more for overtime and this results in a shift of the SRAS to the left. This means that we are at a new equilibrium where output is at the same level and the price level is higher (PL3). This is why this type of growth is short run economic growth. With the Keynesian view, if the economy has a negative output gap, the increase in aggregate demand causes the price level to rise and real output to also rise. If the economy was already producing its long run maximum of output, we would see no change in output and only an increase in the price level.

A classical and Keynesian diagram showing how an increase in demand effects real output and the price level.

A Change in Commodity Prices

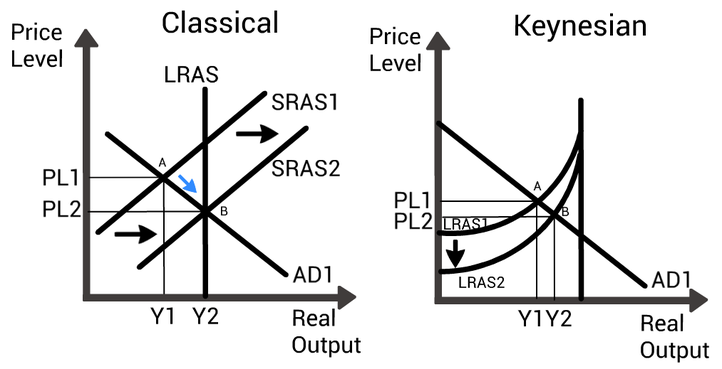

A decrease in the price of world commodities, such as oil, would result in an outwards shift of the SRAS. Economic growth is represented by output increasing from Y1 to Y2. A positive shock would be useful if the economy was experiencing a negative output gap as production can increase.

A decrease in the price of world commodities, such as oil, would result in an outwards shift of the SRAS. Economic growth is represented by output increasing from Y1 to Y2. A positive shock would be useful if the economy was experiencing a negative output gap as production can increase.

And example of how decreases in commodity prices can facilitate short run economic growth.

Output Gaps

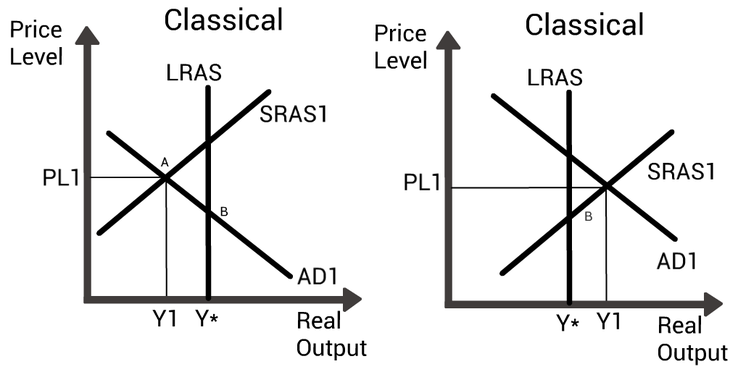

This leads us on to output gaps. Output gaps can either be positive or negative. A positive output gap is where the level of output is greater than the level of output that will be achieved in the long run. Hence, output gaps only apply in the short run. A negative output gap is when output in the short run is at a lower level than it would be in the long run. The classical diagrams indicating a positive and negative output gap are shown below. The positive output gap is shown on the left and the negative output gap on the right.

This leads us on to output gaps. Output gaps can either be positive or negative. A positive output gap is where the level of output is greater than the level of output that will be achieved in the long run. Hence, output gaps only apply in the short run. A negative output gap is when output in the short run is at a lower level than it would be in the long run. The classical diagrams indicating a positive and negative output gap are shown below. The positive output gap is shown on the left and the negative output gap on the right.

Two classical diagrams with a negative output gap on the left and a positive output gap on the right.

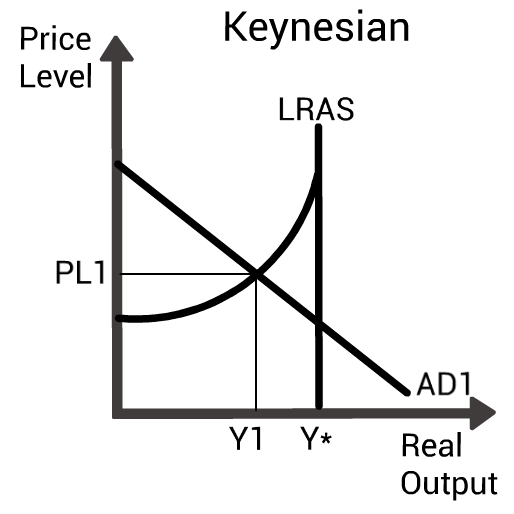

Keynesian economists would say that there will never be a positive output gap, there will only be negative output gaps. The negative output on the Keynesian diagram below is the difference between Y1 and Y*. Y1 is the amount of real output that is being produced and Y* is the maximum amount of output that the economy can produce.

A Keynesian diagram showing a negative output gap.