3.3. COSTS OF PRODUCTION

|

|

In economics we have various periods of time. With regards to the production process we look at the short run and the long run. In the short run we say that at least one factor of production is fixed. Adding more of the variable factors into the production process can increase output. The long run is where all factors of production are flexible.

Firms incur various different types of costs.

Fixed costs – these do not change with the level of production and are expenses that the company has to pay independent of the business activity. One example is rent. Suppose a firm had to pay rent of £40,000 a month for a factory, it still has to pay it whether it produces at full capacity or if it produces nothing. Other examples include business rates, staff that are paid salaries and depreciation of capital (down to age not use). We have both total fixed costs and average fixed costs. Total fixed costs are the sum of all of the fixed costs. Average fixed costs are the total fixed costs divided by the output.

Suppose we have a firm that sells go-karts and it has the following fixed costs (all in per month figures):

1. Rent - £20,000

2. Salaries staff - £15,000

3. Business rate - £5,000

Firms incur various different types of costs.

Fixed costs – these do not change with the level of production and are expenses that the company has to pay independent of the business activity. One example is rent. Suppose a firm had to pay rent of £40,000 a month for a factory, it still has to pay it whether it produces at full capacity or if it produces nothing. Other examples include business rates, staff that are paid salaries and depreciation of capital (down to age not use). We have both total fixed costs and average fixed costs. Total fixed costs are the sum of all of the fixed costs. Average fixed costs are the total fixed costs divided by the output.

Suppose we have a firm that sells go-karts and it has the following fixed costs (all in per month figures):

1. Rent - £20,000

2. Salaries staff - £15,000

3. Business rate - £5,000

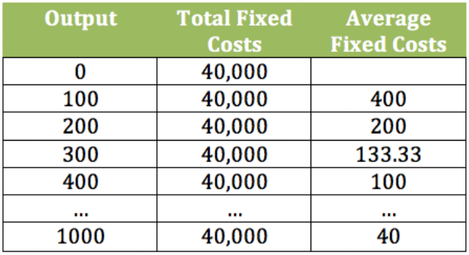

A table show that as output increases the average fixed costs decline.

A table show that as output increases the average fixed costs decline.

Their total fixed costs would be the sum of all the fixed costs (20,000 + 15,000 + 5,000), which comes out to be £40,000. Their average fixed costs are dependent on the amount of output.

As you can see from the table the greater the output that the firm produces the lower the average fixed costs become, in the short run. But the total fixed costs will always stay the same no matter how much is produced.

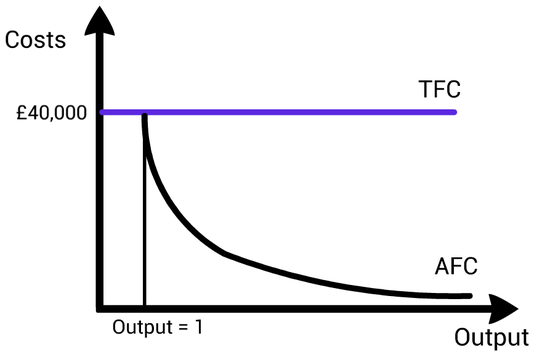

Fixed costs are one area that can allow a firm to achieve economies of scale because a company can reduce their average fixed costs with the greater quantity that they produce, meaning that profit margins per item will be higher resulting in higher profit. From the table you can see that if this company produces more go karts its average fixed costs fall. If it chooses to product 200 go karts then the average fixed cost is £200 but if the firm increases its production then the fixed costs are spread over more units resulting in the average fixed costs falling. Suppose the production of go-karts increased to 1000 per month, the average fixed costs would fall to £40. The total fixed costs (TFC) and average fixed costs (AFC) are plotted on a graph below.

A graph plotting the average fixed costs and total fixed costs from the table above.

As you can see from the table the greater the output that the firm produces the lower the average fixed costs become, in the short run. But the total fixed costs will always stay the same no matter how much is produced.

Fixed costs are one area that can allow a firm to achieve economies of scale because a company can reduce their average fixed costs with the greater quantity that they produce, meaning that profit margins per item will be higher resulting in higher profit. From the table you can see that if this company produces more go karts its average fixed costs fall. If it chooses to product 200 go karts then the average fixed cost is £200 but if the firm increases its production then the fixed costs are spread over more units resulting in the average fixed costs falling. Suppose the production of go-karts increased to 1000 per month, the average fixed costs would fall to £40. The total fixed costs (TFC) and average fixed costs (AFC) are plotted on a graph below.

A graph plotting the average fixed costs and total fixed costs from the table above.

A graph plotting the average fixed costs and total fixed costs from the table above.

A graph plotting the average fixed costs and total fixed costs from the table above.

However, it is worth noting that fixed costs are only fixed over a certain range of production. As you increase production you may reach the capacity of your factory so fixed costs will have to increase to accommodate this demand. Suppose that this factory could only produce a maximum of 2000 go-karts and the firm wanted to increase production to 2,500. This would result in the firm having to rent or buy a new factory, which would then increase the firms total fixed costs (and thus affect the average fixed costs).

There is another type of cost and these are variable costs. Variable costs depend on the level of production. As production increase the variable costs increase and as production falls the variable costs decrease. It a firm produces no output then the variable costs for this firm will be 0. The firm will still experience fixed costs as fixed costs do not change with respect to the level of production. Variable costs include material costs and labour costs (those who are not on a salary), which are necessary to complete production. A pizzeria would have the variable costs of anything that is needed to make pizza; such as flour, yeast, olive oil, cheese, ham, peperoni, the electricity used for production, the labour needed (labour not on salaries) and the capital depreciation of the machinery (caused by use not age).

Managers and owners of businesses need to have an idea about their fixed and variable costs so that they know how much they need to charge for their good/ service if they increase or decrease their output

There is another type of cost and these are variable costs. Variable costs depend on the level of production. As production increase the variable costs increase and as production falls the variable costs decrease. It a firm produces no output then the variable costs for this firm will be 0. The firm will still experience fixed costs as fixed costs do not change with respect to the level of production. Variable costs include material costs and labour costs (those who are not on a salary), which are necessary to complete production. A pizzeria would have the variable costs of anything that is needed to make pizza; such as flour, yeast, olive oil, cheese, ham, peperoni, the electricity used for production, the labour needed (labour not on salaries) and the capital depreciation of the machinery (caused by use not age).

Managers and owners of businesses need to have an idea about their fixed and variable costs so that they know how much they need to charge for their good/ service if they increase or decrease their output

Total costs (TC) = fixed costs + variable costs

Average Total Costs (ATC) is the total costs divide by the output level.

ATC = Total Costs (TC) / output (Q)

Average Total Costs (ATC) is the total costs divide by the output level.

ATC = Total Costs (TC) / output (Q)