2.6 Supply

|

This video is relevant for this section despite it saying that it is for AQA.

|

|

Supply is the quantity of a good or service that a producer is willing and able to supply to the market at a given price over a given period of time”. The supply curve maps out how a change in price will affect how much of a good or service producers are willing to supply.

|

The ‘normal’ supply curve is upwards sloping from left to right, but why is this? One reason is that higher prices imply higher profits and this provides an incentive for firms to expand their production. Also, this higher price sends a signal to other firms to enter into the market and overall output increases.

Another reason is to do with production costs. This is something that I will touch upon later in more detail. As a firm increases production, they experience diminishing marginal returns from the additional factors of production that they add. This means that increasing their production of a good is more costly and these costs have to be covered by having a higher price. As the price increases the firm is then able to increase its production, as the new price will cover the cost of the additional production.

Another reason is to do with production costs. This is something that I will touch upon later in more detail. As a firm increases production, they experience diminishing marginal returns from the additional factors of production that they add. This means that increasing their production of a good is more costly and these costs have to be covered by having a higher price. As the price increases the firm is then able to increase its production, as the new price will cover the cost of the additional production.

Movements Alone Vs Shifts in SupplyAs with demand, a change in the price results in a movement along the supply curve, either a contraction (moving down the supply curve) or an expansion (which is moving up the supply curve). We can also have shifts of the supply curve that come about by various factors:

- A change in technology. An advance in technology would increase the productivity in a firm. Productivity is a measurement of inputs to outputs. If productivity rises, then a firm is able to produce more output from a given amount of inputs. This lowers the cost of each unit produced, meaning that the firm is able to supply more of certain goods at the same price level. And this is represented by an outwards shift of the supply. Any productivity improvement or technological advancement will have this effect (of an outwards shift in supply).

- A change in the production costs. The best example of a production cost would be oil. Oil is in composite demand meaning that it is demanded for many different uses. A change in the price of oil would affect the majority of firms because firms need oil for the transportation of goods, or to use oil for plastics etc…. An increase in the price would make production for firms more costly. This would mean that they will be less willing to supply goods to the market (or for the same quantity they would demand a higher price), which means that there would be a shift to the left of the supply curve. The opposite could be said now as oil price have fallen a large amount since its peak in 2008. This price fall results in production becoming cheaper and the supply curve will shift to the right.

- Government policy relating to taxes and subsidies will have an effect if they are placed on the producer rather than the consumer. A subsidy would shift the supply curve to the right and a tax would shift the supply curve to the left.

Supply Schedule

Similar to demand we can have a supply schedule. A supply schedule shows the quantity that firms are willing and able to bring to the market at a given price over a given period of time.

Similar to demand we can have a supply schedule. A supply schedule shows the quantity that firms are willing and able to bring to the market at a given price over a given period of time.

Producer Surplus

|

Producer surplus is the difference between what producers are willing to supply a good for and the price that they receive for that good. Producer surplus is a component of economic welfare along with consumer and government surplus.

|

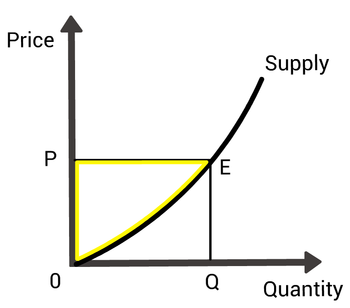

If the price in this market was P and we have the supply curve 'supply', the area for producer surplus is 0PE (which is the yellow triangle).

If the price in this market was P and we have the supply curve 'supply', the area for producer surplus is 0PE (which is the yellow triangle).

Suppose that we have the same supply curve as before but we extended it slightly to assume that for a price of zero the firm is willing to supply zero (this is so we can easily see what the area of producer surplus is). Also, let’s suppose that the price that in this market is 30 and for every good that a firm sells, they will receive a price of 30. With a price of 30 we know that the output in this market will be 30 by looking at the supply schedule. Producer surplus is worked out by the additional income that firms get above what they are willing to supply the good at. It is the difference between the supply curve and the price and is represented by the area OPE.

Elasticity of Supply

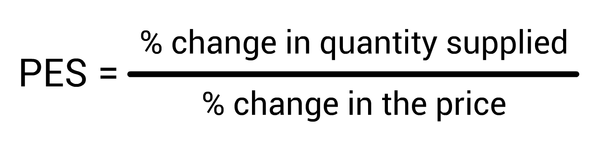

The supply curves shape is dependent on a variety of factors. Price elasticity of supply measures the responsiveness of supply to a change in the price. The formula is:

The supply curves shape is dependent on a variety of factors. Price elasticity of supply measures the responsiveness of supply to a change in the price. The formula is:

The formula for Price Elasticity of Supply.

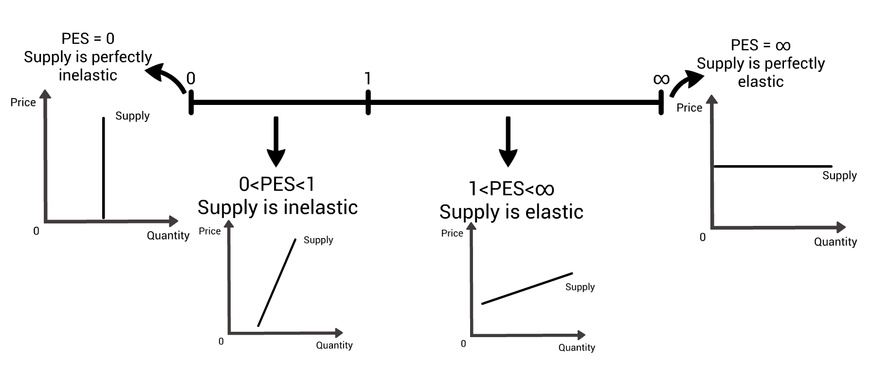

- When PES is greater than 1, supply is elastic. This means that the change in output can be met without a large rise in the price.

- When PES is less than 1, supply is inelastic. This means that supply is relatively unresponsive to a change in demand.

- When PES is 0, supply is perfectly inelastic. This means that output will not change depending on the price of the good. A change in demand will cause a large increase in the price of that good without an increase in output. An example of this could be tickets for a concert or football game. There is only a set capacity and the tickets will be rationed out by who is willing to pay the most.

- When PES is infinity, supply is perfectly elastic. This is where a firm will produce as many goods as individuals demand providing the price that they desire has been paid.

What supply curves with different values of PES look like.

Here are some numerical examples. Suppose that the price in a market increases by 10% and this cause firms to be willing to increase their output from 100 to 140. The increase in output by firms is 40% (((140-100)/100)*100). Price elasticity of supply is worked out by dividing the % change in quantity supplied by the % change in price. This results in PES equaling 4 (40%/10%). A value of PES of 4 means that supply in this market is elastic.

What effects PES?

There are many factors that effect price elasticity of supply. Here are a few:

There are many factors that effect price elasticity of supply. Here are a few:

- Spare capacity: if firms have spare capacity, then they can easily increase output without a huge rise in costs. In a recession, firms tend to produce below full capacity resulting in the supply of goods and services becoming more elastic (through operating on the more elastic part of the supply curve. Remember Elasticities are constantly changing along the supply curve unless the supply curve is unitary elastic).

- Stock levels: some industries have higher levels of stocks than others. These industries are able to accommodate small increases in demand for that good without a huge rise in prices, meaning the supply curve would be elastic.

- Number of producers: the more producers there are, the easier it is to increase production of that good. Supply would be more elastic.

- Availability of resources: if an economy is using the majority of its scarce resources, then firms will find it difficult to employ more. This means that output will not be able to rise. Also, the cost of employing these new resources would increase resulting in the increased cost being passed onto consumers.

- Time period: the supply period and production speed have an effect on the price elasticity of supply. The longer a firm is allowed to adjust its production levels the more price elastic supply will be. The supply of eggs is fairly price elastic as there is a short time span from chickens producing eggs and egg related products reaching the market place. Whereas, in agriculture the momentary supply is fixed as it has been determined by planting decisions months before and climate decisions affect production yields. The price elasticity of supply would be very inelastic or perfectly inelastic for these types of goods (examples are wheat, carrots).